Lending Systems and UX Design: A UK-UAE Comparison

A comparative study exploring regulatory landscapes, credit systems, and bilingual UX design to scale a product like Loqbox across diverse markets.

Index:

1. Comparative Analysis of Lending Policies and Regulations

2. Credit Score Systems and Their Impact

3. Loan Documents Compared

4. Product Localization: English vs Arabic Versions

5. UI/UX Design Considerations: LTR vs. RTL

Industry

Fintech

Product type

Lending

Role

Product Research

User Research, Interaction, Visual design, Prototyping & Testing

Overview

This case study explores the opportunities and challenges of adapting a lending product similar to Loqbox for the UAE market, focusing on regulatory, credit, and UX design differences between the UK and UAE. As the lead designer at a Bristol-based FinTech committed to ending financial exclusion, I was driven by our UK success, including a 4.5★ Trustpilot rating and multiple SPARKies awards, to explore global expansion. The UAE, with its digitally engaged, financially literate Arabic-speaking population, emerged as a promising new horizon.

The study compares the UK's Consumer Duty and Breathing Space policies with the UAE’s Shari’a-compliant lending models and debt relief initiatives, uncovering how local regulations shape user trust and adoption. It also contrasts credit scoring systems to reveal differing expectations around transparency and accessibility. A core focus is the design complexity of creating a bilingual experience, shifting from Left-to-Right (LTR) English to Right-to-Left (RTL) Arabic, while maintaining intuitive, culturally sensitive interfaces.

Through this comparative lens, the research identifies scalable strategies for FinTech platforms to enter diverse markets while remaining compliant, usable, and inclusive. Ultimately, it serves as a roadmap for building lending products that are both locally relevant and globally competitive, with design at the heart of cross-market success.

Comparative Analysis of Lending Policies and Regulations

UK

Regulatory Body: Financial Conduct Authority (FCA)

Key Regulations:

Consumer Duty: Mandates firms to prioritize consumer interests, ensuring fair treatment and transparency.

Breathing Space Scheme: Provides individuals with temporary relief from debt enforcement, allowing time to seek advice and develop repayment plans.

Pre-Contractual Information: Lenders must provide clear details on loan terms, interest rates, and fees before agreement.

UAE

Regulatory Body: Central Bank of the UAE (CBUAE)

Key Regulations:

Consumer Protection: Emphasis on transparency and fairness, with specific regulations for short-term lending products.

Bankruptcy Law (Effective May 2024): Introduces structured processes for debt restructuring and insolvency.

Pre-Contractual Information: Mandatory disclosure of comprehensive loan details, including Annual Percentage Rate (APR) and fees.

Credit Score Systems and Their Impact

What's the score?

Credit scores are the backbone of lending products. They determine a user’s creditworthiness and directly affect loan eligibility, interest rates, and financial access. While the UK uses scores from bureaus like Experian, Equifax, and TransUnion, the UAE relies on the Al Etihad Credit Bureau. Though the scoring ranges vary by region, the goal remains the same: predict risk and build trust in a user’s ability to repay.

So what?

When designing a lending app, understanding these systems is crucial. It helps tailor features like progress tracking, credit education, and personalized recommendations. A product like Loqbox can guide users through improving their scores by simplifying complex concepts, showing tangible benefits, and celebrating small wins. Localization both in language and financial behavior is key to building trust and encouraging long-term engagement across different regions.

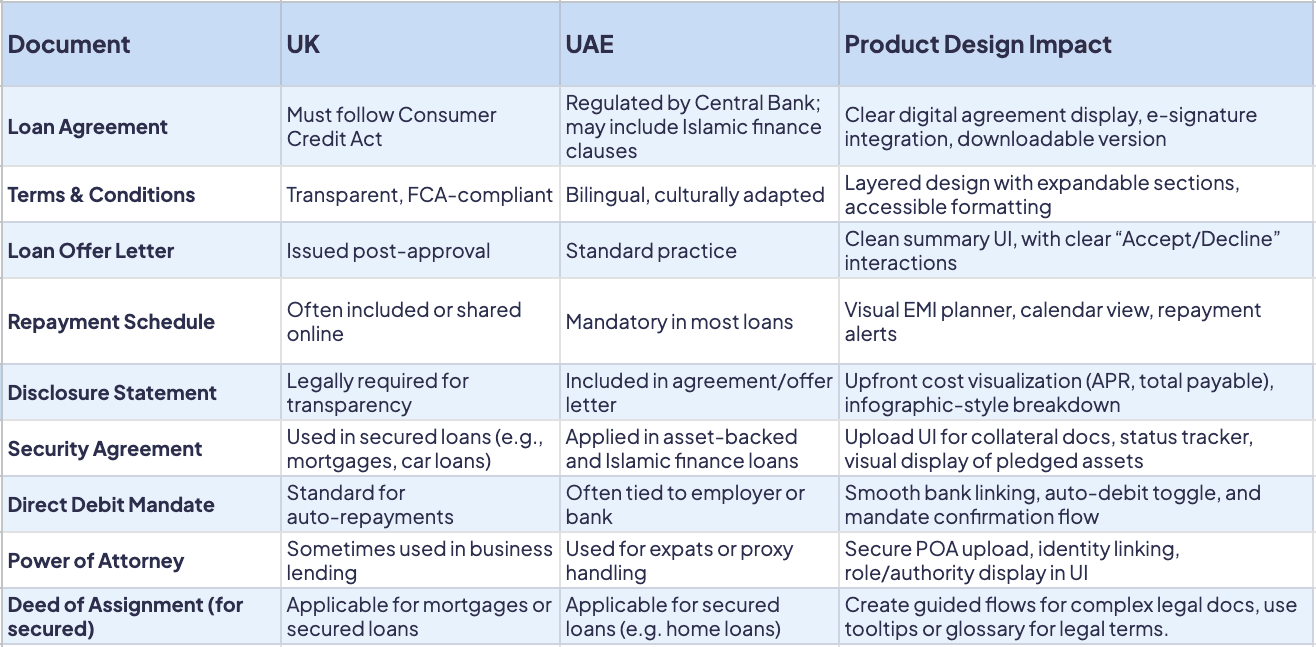

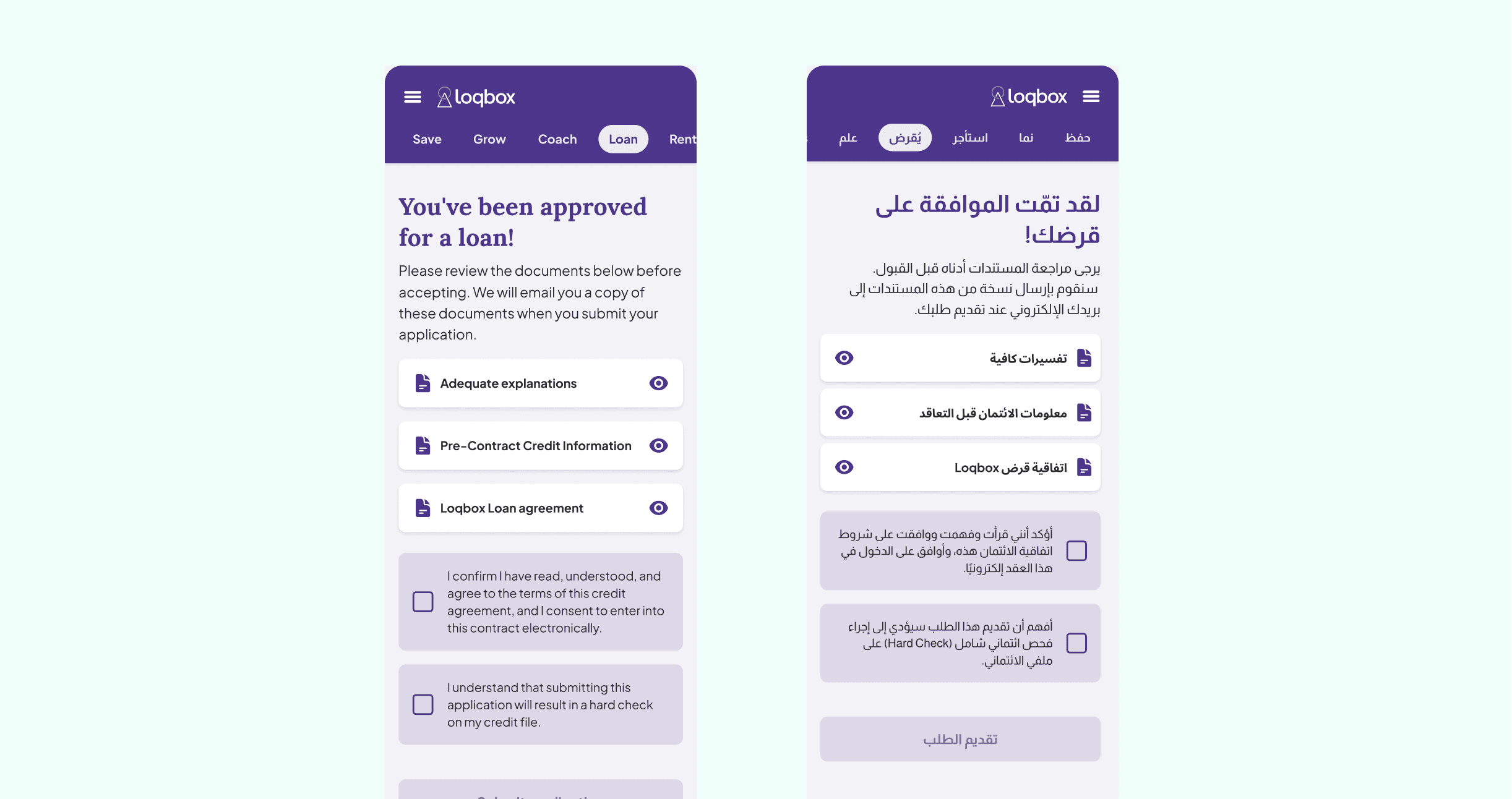

Loan Documents Compared

What's the docs?

Loan documents are the official papers that explain the details of a loan. These include the loan agreement, terms and conditions, offer letter, repayment schedule, and sometimes additional forms like a direct debit mandate or power of attorney. They cover important information such as how much you’re borrowing, how much interest you’ll pay, when payments are due, and what happens if you miss one. In countries like the UK and UAE, the format and rules for these documents can vary, including things like language requirements or religious finance guidelines.

So what?

Designers play a big role because they decide how users see and interact with loan information. If the design is confusing or hard to read, users may not understand important details about their loan. This can lead to mistakes, lost trust, or even legal problems. A good design makes complex terms simple, shows payment plans clearly, and helps users feel confident. Designers also need to think about different users, languages, and rules in each country. For example, in the UAE, some users may need Arabic text and Sharia-compliant layouts. By designing with care, they help create a smooth, honest, and legal user experience.

Product Localization: English vs Arabic Versions

Why Localization?

Builds trust with native users

Improves comprehension, especially in financial terms

Complies with cultural and linguistic norms

Increases adoption in non-English speaking regions

Boosts accessibility and user satisfaction

Image: A colored map showing countries with Arabic dialects. Source: Wikipedia

Why Arabic?

Arabic is the official language of the UAE and widely spoken across the MENA region.

420 million Arabic speakers worldwide; Arabic is the 5th most spoken language globally.

Arabic users in the UAE expect fully localized experiences—not just translated copy.

Cultural relevance increases trust, engagement, and conversion rates in financial products.

UAE residents include a large local and expat Arab population who prefer to interact in Arabic, especially for financial decisions.

Government services and major banks already offer fully localized Arabic interfaces — users expect the same from digital products.

Any research/Proof?

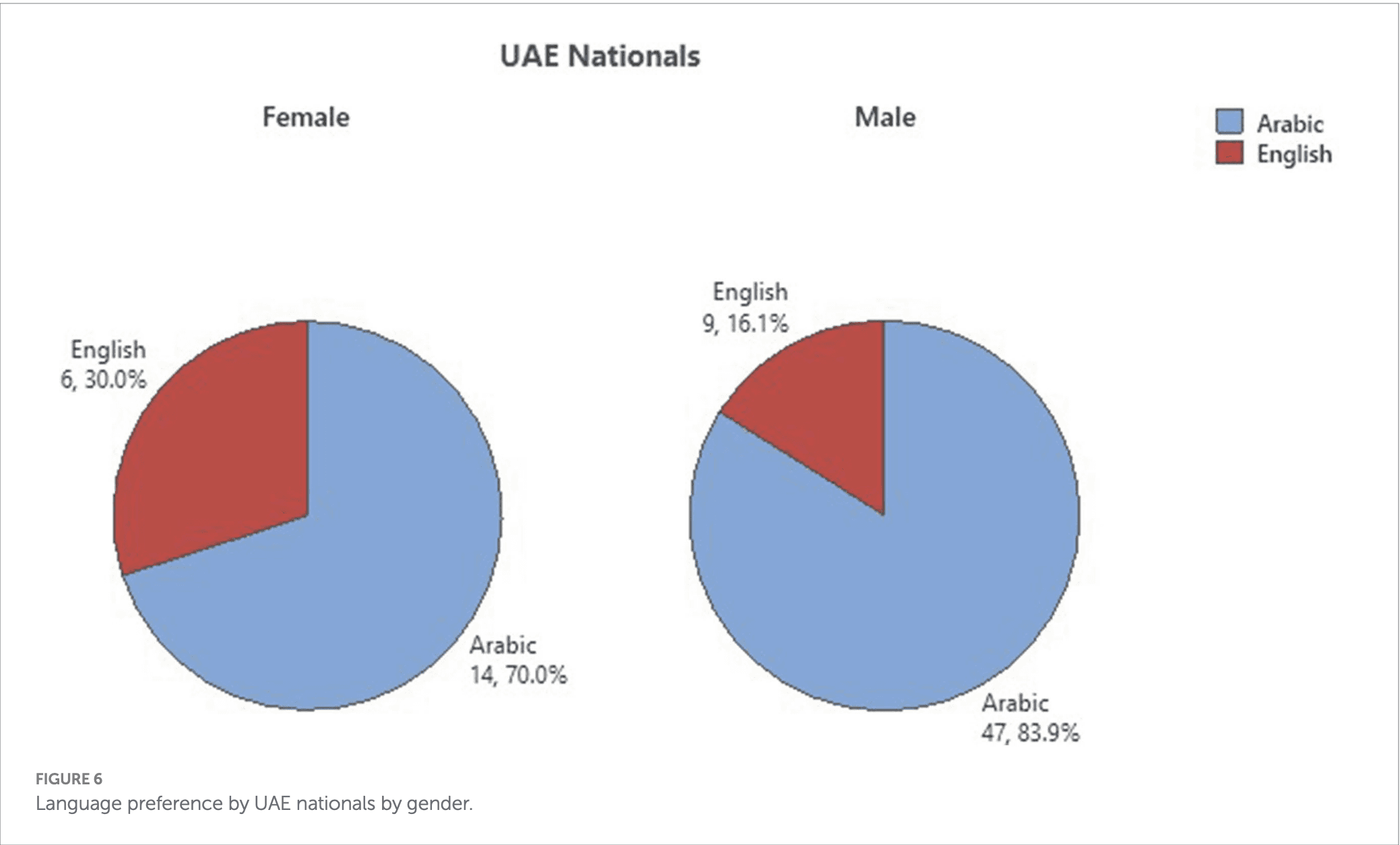

To strengthen the case for Arabic localization, I referred to the academic study "Arabic or English? Multilingual Users’ Preferences in Dubai ATM Transactions" by Ahmad Al-Issa and Hana Sulieman. This study surveyed 566 participants in Dubai to explore how users interact with technology in Arabic vs English.

59.3% of Arab users prefer Arabic for ATM transactions

72.2% of Arabs outside Dubai prefer Arabic, showing even stronger regional demand

Among less tech-savvy users, 85.2% prefer Arabic

In lower-income jobs, 84.3% prefer Arabic, compared to only 31% in higher-paid roles

While 99.7% of non-Arabs prefer English, Arabic remains critical for native user groups

This data highlights the need for a bilingual (English and Arabic) experience, especially in financial platforms targeting accessibility and inclusion. It reinforces the idea that Arabic isn’t just a nice feature, It’s necessary, especially for people with low-income money or who aren’t used to using technology, which aligns closely with Loqbox’s mission to promote financial inclusion for all.

Image 2: A piechart showing Language preference by Arabs.

Image 3: A piechart showing Language preference by UAE nationals by gender.

Source: Researchgate

Key insights:

User Group | Arabic Preference | English Preference |

|---|---|---|

Arab participants | 59.3% | 40.7% |

Arabs outside Dubai | 72.2% Arabic | 27.8% English |

Tech-uncomfortable Arabs | 85.2% Arabic | 14.8% English |

Lower-income jobs | 84.3% Arabic | 15.7% English |

Higher-income jobs | 31% Arabic | 69% English |

Non-Arabs | 0.3% Arabic | 99.7% English |

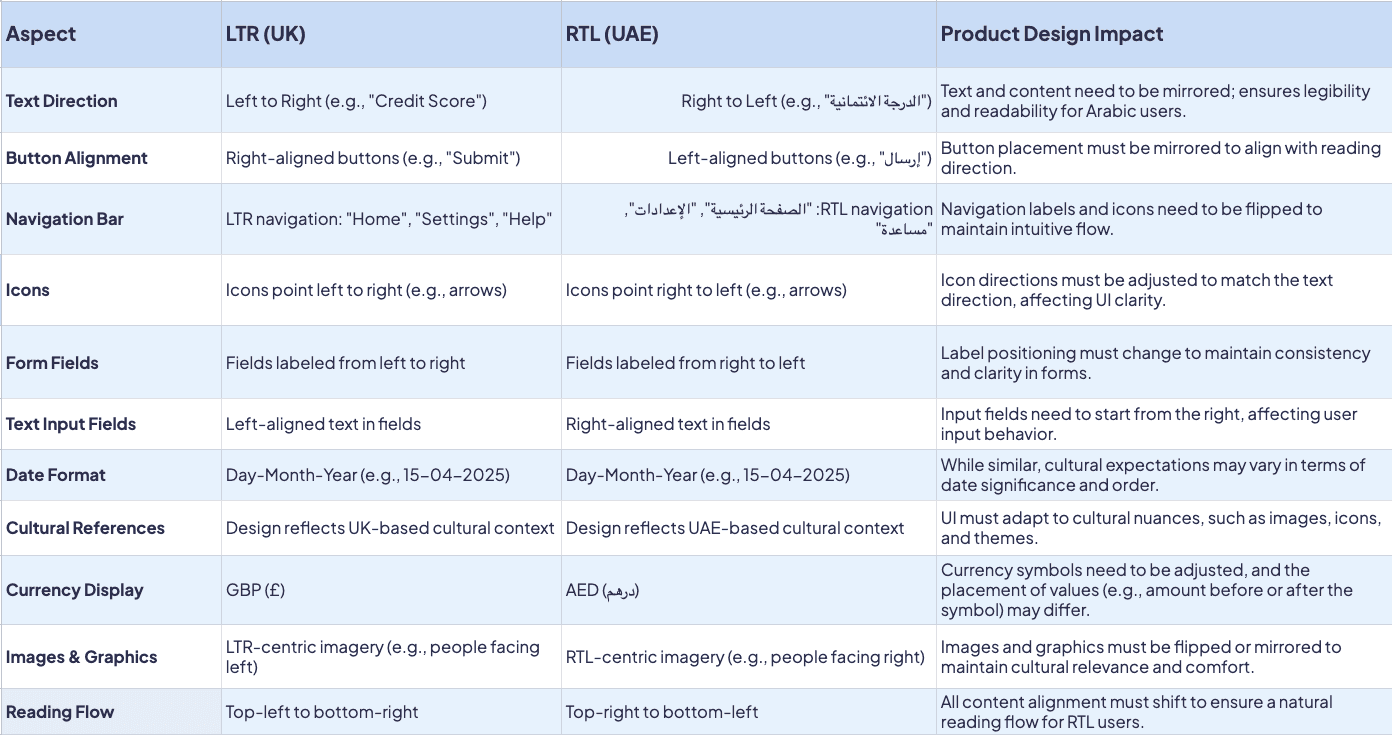

UI/UX Design Considerations: LTR vs. RTL

Layout and Navigation:

LTR (English): Content flows from left to right; primary navigation typically on the left.

RTL (Arabic): Content flows from right to left; primary navigation on the right.

Design Elements:

Text Alignment: Adjust text alignment to match reading direction; right-aligned for Arabic.

Icons and Imagery: Mirror directional icons to align with reading flow. something similar to arrows/arrow icons.

Typography: Select fonts that support Arabic script and maintain readability.

User Behavior:

Arabic users often scan pages starting from the top right, mirroring the F-shaped pattern observed in LTR languages.

Design should respect cultural norms, such as color symbolism and imagery appropriateness.

Some of the guidelines can be found at RTL Apple developer documentation: Link here.

A quick translation of the existing designs of Loqbox Loan to Arabic. Full Figma design file here.

If I can start working on a project for UAE:

1. Understanding the Market Landscape

The UAE's fintech sector is experiencing rapid growth, with projections estimating the market to reach USD 6.43 billion by 2030, growing at a CAGR of 12.56% . This growth is fueled by high smartphone penetration, a tech-savvy population, and supportive government initiatives. However, the market is diverse, comprising both local Emiratis and a vast expatriate community, each with distinct financial behaviors and needs.Mordor Intelligence

2. Cultural and Linguistic Localization

Arabic is the official language of the UAE, and a significant portion of the population prefers using services in Arabic. Designing for Right-to-Left (RTL) languages requires more than just mirroring layouts; it involves rethinking navigation flows, iconography, and content hierarchy to ensure intuitive user experiences. Additionally, incorporating culturally relevant themes and avoiding content that may not resonate with local values is crucial.

3. Regulatory Compliance and Financial Ethics

The UAE's financial sector is governed by strict regulations, including those aligned with Islamic finance principles. Products must comply with Shariah laws, avoiding interest-based earnings and ensuring ethical investment practices. Collaborating with local legal experts and Shariah scholars would be essential to ensure the product's compliance and acceptance in the market.UAE Stories

4. Building Trust through Transparency

Trust is paramount in financial services. Given the diverse user base, it's vital to provide clear, concise, and transparent information about financial products. This includes straightforward terms and conditions, easy-to-understand fee structures, and accessible customer support in both Arabic and English. Implementing features like real-time transaction notifications and personalized financial advice can further enhance trust and user engagement.PwC

5. Leveraging Technology for Personalized Experiences

With the UAE's high digital adoption rate, integrating advanced technologies like AI and machine learning can offer personalized user experiences. For instance, AI-driven insights can help users manage their finances better by analyzing spending patterns and suggesting savings plans. Moreover, incorporating biometric authentication methods can enhance security and user convenience.

6. Iterative Design and Continuous Feedback

Launching a product in a new market necessitates an iterative design approach. Regularly collecting user feedback through surveys, usability tests, and analytics will help refine the product to better meet user needs. Engaging with local communities and conducting focus groups can provide deeper insights into user expectations and preferences.

Learnings and Conclusion

This research journey has been eye-opening. As I compared the lending landscapes in the UK and UAE, I realized that building a financial product isn't just about features and functions. It's about deeply understanding the environment people live in, the rules that shape their choices, and the language that makes them feel secure.

I learned that policies like the UK’s Consumer Duty or Breathing Space create a very different financial mindset compared to the UAE's Sharia-compliant, culturally rooted systems. I also saw how credit scoring awareness varies. In the UK, people regularly check their score through services like Experian or ClearScore, while in the UAE, the credit ecosystem is newer and evolving around AECB.

One of the biggest takeaways for me was the role of language. Arabic isn’t just a translation need. It's essential for clarity, confidence, and inclusion, especially for users who may not be comfortable with English or financial jargon.

From regulation and credit awareness to UI patterns and localization, every layer of this case study taught me that real innovation starts with empathy. If a fintech wants to scale successfully in the UAE, it must do more than enter a market. It must truly understand and serve it. This project gave me the clarity, curiosity, and cultural awareness to move forward with confidence.